Staying on top of cash flow should be the biggest priority for most businesses.

But it's easier said than done if you’re one of the 63% of small businesses who are in the dark about their earnings. The good news is, you can buck this trend and get more clarity into your financials by learning to use multiple bank accounts for budgeting. And in this guide, we'll show you how to implement this type of budgeting system in your business.

How does multiple bank account budgeting work?

Multiple bank account budgeting works by opening dedicated checking accounts for different expense categories and reserve funds, then allocating specific amounts of cash to each one. You need a clear picture of your expense types and how to categorize them. Once set up, a quick glance tells you whether you have enough for each category.

It's like the envelope budgeting method—allocating set amounts for different expenses—only digital. Say you want to track taxes, payroll, and operating expenses separately. You'd open three accounts: one for taxes, one for payroll, and one for everything else. When you look at your accounts, you instantly know your position in each category.

Compare this to keeping everything in one account. You see $10,000 in your balance. But how much goes to contractors? How much is earmarked for taxes? What about rent? With a single account, you rely on mental math and memory to figure out your real cash position. That's where mistakes happen.

This approach also acts as a reporting stop-gap when your financial statements run late. Many businesses prepare reports once a quarter—or not at all. But you make financial decisions daily. Can you afford this purchase? Should you invest in new equipment? You need data to decide wisely.

When you don't have current reports, dedicated accounts provide that data. If you put 15% of every dollar into an account labeled "Taxes—do not touch," you know instinctively that money isn't available for spending. You're far less likely to misallocate it. The Profit First method uses this exact principle to help owners prioritize profitability.

How many business checking accounts should you have?

Most small businesses benefit from 5–7 checking accounts: one primary account for receivables, plus dedicated accounts for operating expenses, taxes, payroll, and emergency reserves. Your exact number depends on how you categorize income and expenses. A service business might need fewer accounts than an e-commerce store managing inventory and multiple vendors.

The right number depends on how you organize your revenue and spending. Retailers may want a dedicated account for supplier payments. Marketing agencies might need a payroll reserve to track labor costs separately. There's no universal answer—only what works for your business model.

Consider both sides of the ledger when planning your accounts. Do you run a YouTube channel with three income streams and want to track each separately? Set up accounts for advertiser payouts, affiliate commissions, and merchandise sales. You'll see at a glance which revenue source is strongest.

Your business type shapes your expense accounts too. E-commerce stores might split inventory expenses from software costs. Short-term rental operators might create an account for each property, plus one dedicated to contractor payments. The article on how many business checking accounts you should have breaks down these decisions in more detail.

Below are common checking account categories to spark ideas for your setup.

Primary checking account

Every business needs a primary account to receive incoming payments. If you organize cash into dedicated expense and reserve accounts, you won't use this account to send money out. Instead, you'll transfer funds from here into those dedicated accounts. Make sure this account handles basic operations like direct deposits and withdrawals.

Operating expenses

Use this account to cover monthly expenses—the day-to-day costs of running your business. Operating expenses typically include rent, software subscriptions, utilities, and travel. You might break this down further depending on your needs. An e-commerce business could open a separate account for software subscriptions and issue a dedicated debit card for it, making expense tracking simpler.

Emergency fund

Businesses that run out of cash face hard choices: layoffs, skipped owner pay, asset liquidation. An emergency fund creates a buffer against this scenario. Set aside a small percentage of monthly revenue and reserve it for unexpected situations or expenses. Start small—consistency matters more than the initial amount. Over time, your emergency fund grows. This safety net helps you avoid credit card debt and protects your personal finances. The guide on how much cash a business should keep in reserve provides specific benchmarks for different industries.

Payroll

Making sure you can cover every payroll cycle gets complicated without visibility into your cash. Nearly 50% of employees start job hunting after two paycheck errors, so tracking payroll funds separately matters. Dedicate one account to payroll and fund it regularly with enough to cover a full month of employee pay, contractor pay, and your own salary. At a glance, you'll know if you're short and can even automate the entire process.

Savings goals

Saving as a business is one of the smartest things you can do. To stay on track toward financial goals—a down payment on equipment, a new vehicle, a hiring budget—set up a separate savings account. Store away the cash you need to meet short-term or long-term objectives. If your goal is to increase savings by 5% this year, set up automatic transfers and allocate 5% of revenue here every month. Keep this separate from your emergency fund—they serve different purposes.

Travel

If you travel frequently for business, a separate travel account helps you set aside the right amount of cash and simplifies deductions at tax time. You can issue dedicated debit cards and assign them to this account, making it easy to track spending on the road. Strong cash flow management means knowing exactly where every dollar goes—even when you're away from the office.

Taxes

Taxes catch business owners by surprise more often than almost any other expense. Failing to save enough for the IRS is one of the most common mistakes. A dedicated tax account prevents this. If you do nothing else, open a second checking account just for tax withholdings—separate from your spending account. If your business brings in $10,000 a month and you pay 15% in taxes, store away $1,500 monthly in your tax account. When tax season arrives, you know you have the cash ready.

What does a multiple bank account budget look like in practice?

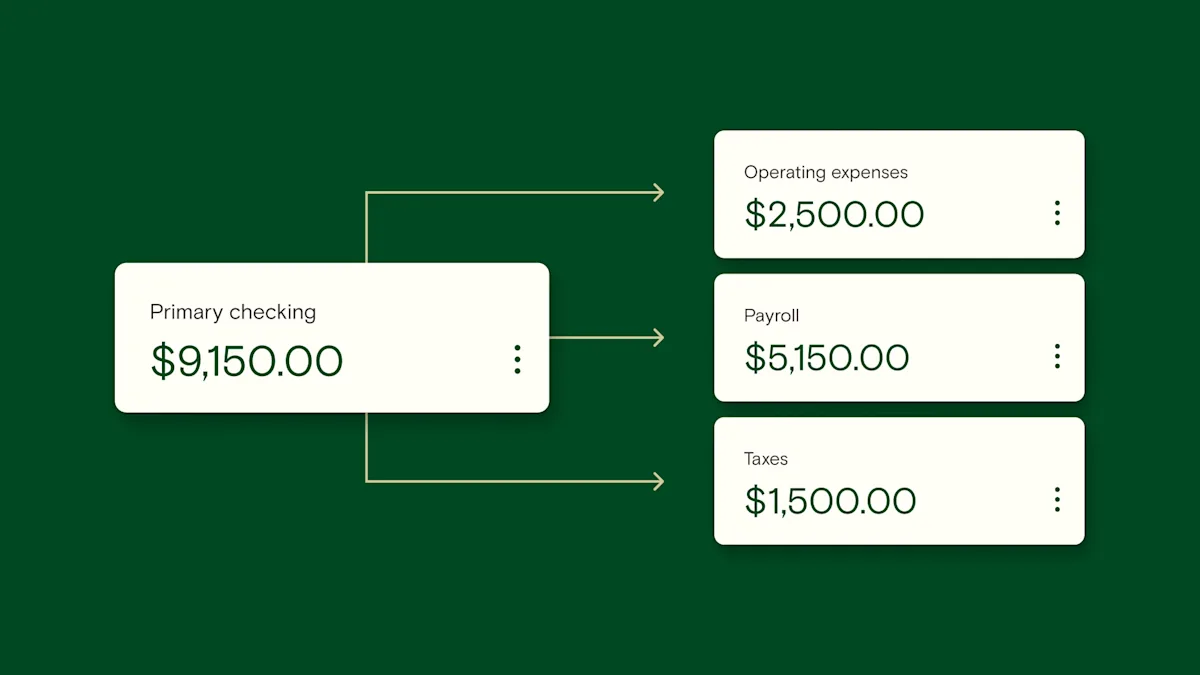

A practical example helps clarify how these accounts work together. Say you own a small service business bringing in $10,000 monthly. You've set up seven business checking accounts to categorize cash flow and gain clarity into spending: primary checking, operating expenses, emergency fund, payroll, savings goals, travel, and taxes.

You transfer all funds from your primary account to the dedicated expense and reserve accounts at the end of each month. At the start of the next month, you can see at a glance how much you have to cover expenses.

Here's what your cash allocations might look like:

Checking account | Transfer rule | Amount at month start |

Primary checking | Receivables. Allocate funds to other accounts at month start. | $0—just allocated to other accounts |

Operating expenses | Funds to cover operating costs | $2,500 |

Emergency fund | 2% to build emergency reserves | $200 |

Payroll | Funds to cover one month of payroll | $5,150 |

Savings goals | 2% for savings objectives | $200 |

Travel | Estimated travel budget | $450 |

Taxes | 15% for estimated taxes | $1,500 |

Suppose it's nearly month-end and you check your primary account—where you receive income—and see only $2,000. This immediately signals a problem. Maybe you're waiting on a client payment, or sales dipped this month. Either way, multiple accounts let you catch this early and develop a strategy to address it. The 9 financial reports every owner needs can help you dig deeper into what's causing the shortfall.

What are the benefits of using multiple bank accounts for budgeting?

Using multiple bank accounts to categorize cash flow gives you greater visibility into how you spend money. Once you have this financial visibility, you make better strategic decisions about resource allocation. You see problems before they become crises. You know when you can invest and when you need to pull back.

Here are the main benefits:

Greater visibility into your current cash position. Digital banking gives you real-time insight into what you're earning, spending, and saving—no waiting for monthly statements.

Easier to stay within your budget. Categorizing expenses makes it simple to see if you're on track. Multiple bank account budgeting isolates categories so cash flow issues in one area don't spill into another.

Easier to save for taxes. Small business taxes get complicated, but saving in a separate account simplifies things. When it's time to pay the IRS, you won't be caught off guard.

Faster bookkeeping. You already know which expense categories associate with which account, so reconciliation goes faster. Direct integrations with accounting software speed things up even more.

More secure. Using one checking account for receivables and allocating funds to dedicated expense accounts keeps your information private and organized. Online banking provides more security tools than traditional methods.

Relay lets you open up to 20 checking accounts1—each with its own account number—so you can put this into practice from day one. Relay has no hidden fees or minimum balance requirements. Open your account in minutes.

1Relay is a financial technology company and is not an FDIC-insured bank. Banking services provided by Thread Bank, Member FDIC. FDIC deposit insurance covers the failure of an insured bank. Certain conditions must be satisfied for pass-through deposit insurance coverage to apply.

Frequently asked questions

How many bank accounts should a small business have?

Most small businesses benefit from 5–7 checking accounts: one primary account for receivables, plus dedicated accounts for operating expenses, taxes, payroll, and emergency reserves. Your exact number depends on how you categorize income and expenses. A service business might need fewer accounts than an e-commerce store managing inventory and multiple vendors.

Does having multiple business bank accounts affect my credit score?

No. Opening or closing business checking accounts does not impact your personal or business credit score. Banks do not report checking account activity to credit bureaus. Only credit products like business credit cards or loans affect your credit score.

Can I use multiple bank accounts for budgeting if I'm a sole proprietor?

Yes. Sole proprietors can open multiple business checking accounts and use them to separate operating expenses, taxes, and savings. This method works regardless of your business structure. Just make sure you're using business accounts, not personal ones, to keep your finances separate.

How do I decide what percentage of income goes into each account?

Start by reviewing your profit and loss statement to see your actual spending patterns. A common starting point: 30% for taxes, 30% for operating expenses, 20% for payroll, 10% for reserves, and 10% for owner pay. Adjust based on your business model and tax obligations.

What's the difference between an emergency fund and a savings account for a business?

An emergency fund covers unexpected expenses like equipment breakdowns or sudden revenue drops. A business savings account is for planned goals like new equipment purchases or expansion. Emergency funds should be liquid and untouched unless necessary. Savings accounts can be used for scheduled investments.