And if I do, who should I bank with? There are thousands of financial institutions in the United States, so choosing the right one for your business can get overwhelming.

Here at Relay, our mission is to keep small businesses on the money with banking that gives you real visibility into what you're earning, spending and saving. Because of this, we get to see first-hand how countless businesses choose to manage their finances, what works and what doesn't. So in this quick overview, we'll take you through how to choose the right bank for your small business. (Note that here we’ll mostly cover business checking accounts, excluding business savings accounts and credit cards.) Let's dive right in! 👇

Why you need a dedicated small business bank account

The IRS recommends that business owners open a separate bank account as soon as they begin making or spending money. This helps avoid commingling funds and helps you keep your records clean. If you're a sole proprietor, you aren’t legally required to have a separate bank account for your business — however, it’s highly advised that you do (more on this later).

Luckily, opening an account for your sole proprietorship is easier than you think — for example, applying for a Relay account takes 10 minutes and can be done completely online.

LLCs and corporations, however, are considered separate legal entities from the business owner, and therefore they require a dedicated business banking account. This helps maintain a separation of funds and protects the business owner from liability.

Whether you're obligated to have a separate business banking account or not, opening one usually comes with features that you simply don't get in personal banking. We'll walk you through some of those features next. But first, you must choose what type of banking account your business needs. 💸

Choosing between traditional and digital banking

When it comes to business checking accounts, there are two main types of banks to choose from: a digital banking account and a traditional, brick-and-mortar bank. There are a lot of differences between digital and traditional accounts — the biggest one being that digital banks operate online, whereas traditional banks operate from a physical branch location. Traditional accounts can be further broken down into big banks and smaller, local credit unions. However, credit unions often offer the same type of services and have a similar approach to large national banks, so they are grouped together here.

A lot of new business owners fall into the trap of simply opening a business account with the same institution where they already have a personal account — which usually means a traditional bank. This can be a costly mistake. 💰

Digital business banking can save your business on fees, and equip you with purpose-built software features that take the pain out of tedious administrative work. The potential downside of using a digital bank may be the lack of branches (if you need in-person services), and a less comprehensive financial services suite compared to traditional banks — as most digital banking platforms are still new.

While it's beyond the scope of this article to discuss the two types of banking solutions in-depth, you can find more information on the differences between digital vs traditional banking here.

Now, let's dive into things to look out for as you evaluate both types of institutions.

🔎 How to choose the right bank for your small business

To choose the right bank for your small business, you'll want to evaluate core banking features, understand the bank's fee structure, and also get a good understanding of what type of business-specific tools that bank offers. 🛠 Because your business banking needs will be much more complex than your personal banking needs, you need a different lens to evaluate each bank. Let’s dig into the most critical business banking features.

💻 Online banking features

Do you expect to get most of your banking tasks done online? Or are you comfortable having to go into a branch? Online and mobile business banking accounts help business owners take control of their finances wherever they are. Some traditional banks also offer online banking features.

You should check if your bank offers a mobile app and whether you can complete banking tasks online or whether you need to visit a branch or phone someone. Being empowered to manage your own money can give you better visibility into cash flow and save you time on needless calls with the bank.

💰 Minimum balance requirements

Finances can fluctuate when building a small business, especially when you’re just getting started. This can put a strain on small businesses and hinder growth, especially if you're trying to budget by opening multiple checking accounts. That’s why it’s important to choose a business bank account that has low to zero minimum balance requirements.

Traditional banks tend to have higher minimum balance requirements, while digital banks offer lower requirements — or none at all. If you bank with Relay, for example, you can open up to 20 free checking accounts per business entity, without ever having to worry about maintaining a minimum balance for it.

💸 Account fees

We know that every expense matters when building a business, and small banking fees can stack up before you know it. The right business bank won’t charge extra account fees or blindside you with hidden costs. This means no monthly maintenance fees, service fees, overdraft fees, or withdrawal fees. (For example, see how Relay approaches pricing here.)

Some banks also have transaction fees in place which apply if you exceed a certain number of transactions each month. It’s important to look out for transaction limits since these can restrict your growth potential.

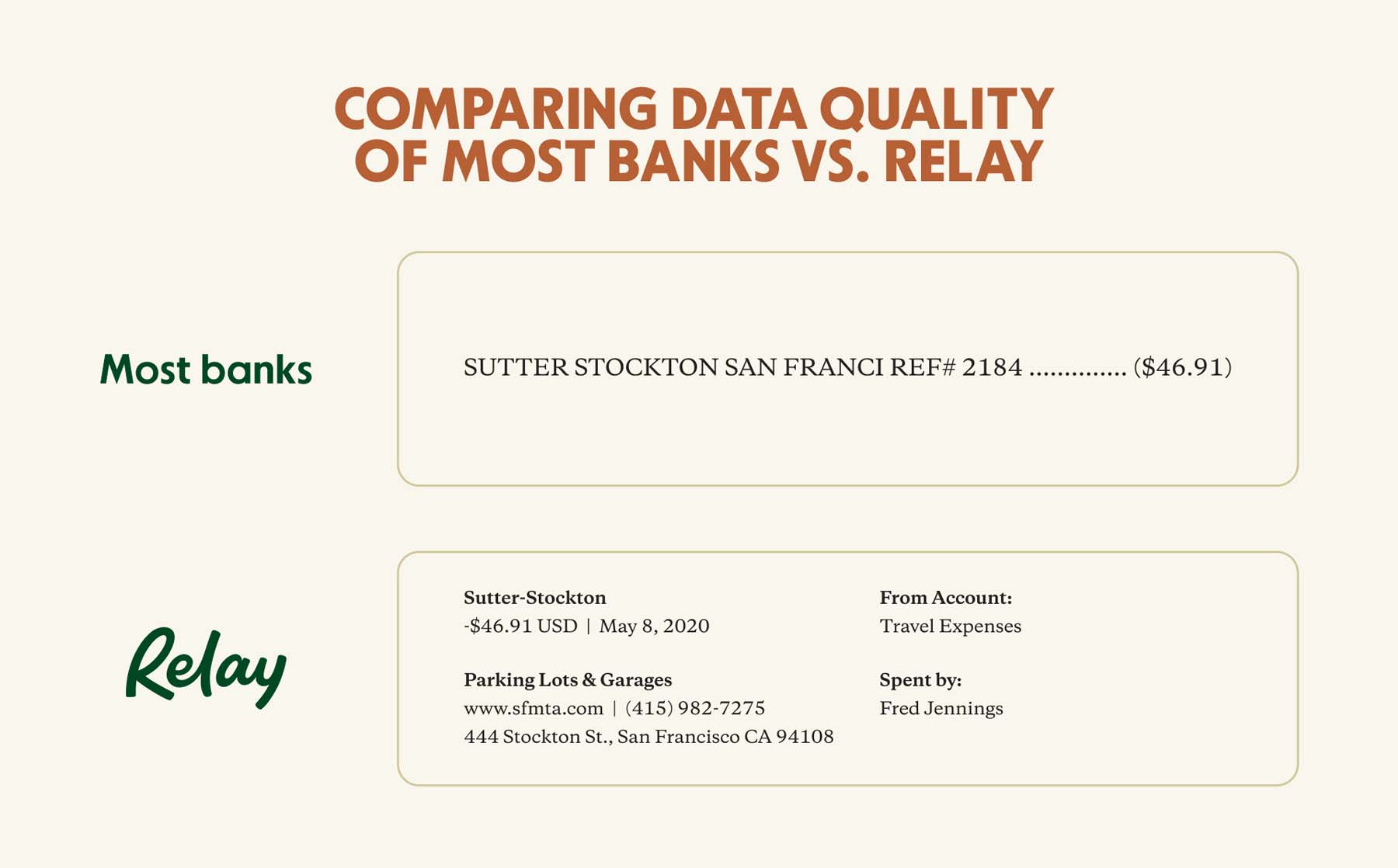

ℹ️ Data quality

Unlike with personal finances, where budgeting and cash management fall under your discretion, when you run a business you have strict reporting obligations. That means you'll need to track your spending and categorize your expenses regularly.

Your bank will either help you do this or make it complicated. It all depends on the quality of data you get about each transaction. Relay, for example, helps you categorize transactions when you're doing bookkeeping because with Relay you get much better-quality data compared to traditional banks.

Better data typically means less time spent on administrative work, better visibility into cash flow, and faster, smarter decision-making about your business.

🤝 Collaboration features

One of the biggest things new business owners forget to consider — especially if they're starting out on their own — is how many different people may need to be involved in their finances and banking.

Whether it's your accountant, your lawyer, or eventual team members, chances are you'll need to collaborate on banking and delegate certain tasks to someone else. Will your bank make it easy for you to do this? Or will you have to jump through hoops to give your accountant banking access? Relay, for example, lets you manage multiple users for every business entity and assign role-based permission levels to each team member who needs to get into banking.

💳 Number of debit cards

As you and your team grow, so will your needs. After all, you don't want to be in a position of having to change business banks because you've outgrown your current institution. One way of future-proofing your business is to ensure you can get multiple business debit cards to distribute to your team. Or, if you're hunting for perks and introductory offers, you may want to look at what business credit cards your potential bank offers instead.

The number of cards each bank offers differs quite significantly, but it’s better to choose an account that offers an abundance of cards rather than too few. With Relay, you get 50 free virtual cards for business spending to issue to your team.

💵 Payments

One of the main banking services entrepreneurs should expect from their business checking account is the ability to make and accept payments. For example, you'll want to know that you can send and receive wire transfers and make ACH payments — and whether your bank will charge you for this or if the payments are included in a free business account.

Also consider whether you'll need to make multiple cash deposits, or if you're running an online business and it's not a concern. While digital banks excel in many areas, they typically aren't great at accepting cash deposits, which is why some businesses choose to keep an account with both a digital and a traditional financial institution.

💰 Lending and lines of credit

For some businesses, banking equates to managing loans and lines of credit and is mostly about having a lender relationship. Are you planning to fund your business with a bank loan? If so, big traditional banks may be a better choice, as digital banking platforms are still catching up in this area. However, with rising interest rates, many businesses are becoming wary of relying on business loans to fuel growth.

🔐 Security

You'll be storing your money in your bank (obviously) — so you want to make sure it's protected. Does your bank offer online access? If so, will your accounts come with two-factor authentication (2FA) enabled? Can you control spending limits? Lock cards or change the PIN number if needed?

All of this should be on your mind as you decide where to keep your money. If you're not sure whether you can depend on online banking to keep you safe, check

💼 Member FDIC insurance

It's a common misconception that FDIC insurance is a legal requirement for US banks. It's not. And while most banks are FDIC insured, some aren't — which is why you should make sure that yours is. FDIC insurance will protect your money in the event of a bank failure, and reimburse you up to $250,000 in the event of said failure. So make sure your chosen institution has this protection.

🔄 Integrations

You probably don't want to spend hours manually transcribing transactions from a PDF bank statement into your accounting software. But without integrations, that's what some banks still expect business owners to do.

To avoid tedious admin work, investigate what accounting software integrations your bank offers. Some popular integrations to look out for are QuickBooks Online and Xero for accounting, and Gusto for managing payroll automation. The right banks will sync transaction data directly into your existing accounting tools and make your (and your bookkeeper's) life much easier.

😊 Customer service

Last but certainly not least, you'll want to make sure you're choosing a bank that has great customer service. After all, banking is one of the most critical parts of your business, so you'll want to make sure you have a team that you can rely on. Customer service is deeply important to us here at Relay so we invest there heavily — and we're proud to have a 4.6 Trustpilot rating and 1200+ reviews as a result!

Congratulations — you now have a better understanding of things to consider to future-proof your choice of bank. Next, let's briefly touch on why you want a business bank account in the first place, and what you'll need to open one.

Benefits of choosing a business bank account

One of the biggest benefits of choosing a business bank account over just using your personal bank account is that you avoid commingling funds. In addition to that, most business accounts will come with additional features — as listed above — that you usually just don't get with personal accounts. To recap, with a business banking account:

Your personal and business finances stay separate. If you're a sole proprietor, separating your personal and business bank accounts will help you with reporting at year-end. And if you run an LLC or a corporation, keeping personal and business finances separate is a requirement.

You get better cash flow visibility: A business account lets cowillllect income in one place so you can see exactly what you’re working with. A crystal-clear picture of your cash flow makes it easy to understand what you’re earning, spending, and saving so you can make the smartest decisions for your business.

Your bookkeeping is simplified: When tax season comes around, a business bank account makes it simple to track revenue and separate business expenses from your personal purchases. Additionally, the right bank may offer pers like accounts payable (bill pay) features to streamline payments further.

What you need to open an account

If you’re ready to open a business bank account, you’ll want to prep the necessary information beforehand. If you choose a digital banking platform like Relay, you can apply online in under 10 minutes. On the other hand, if you choose a traditional bank you may need to make a trip to a branch to open an account.

The documents needed to open a business bank depend on the type of business you own. In general, you’ll need to provide:

🪪 Photo of Government-issued ID

🔢 Social Security Number (SSN)

🏠 Mailing Address

📞 Phone Number

📧 Email Address

For corporations and LLCs, you may need to provide additional information such as your EIN and Articles of Organization. Unlike with a startup loan or credit account, you shouldn’t need to provide a credit score check to open a business checking account.

Choose Relay for your banking needs

Ultimately, the right business bank will grow with you over time. This includes allowing you to open numerous accounts, providing a platform that understands your spending behaviors, and offering unmatched cash flow clarity.

With Relay, you can use up to 20 checking accounts to organize and allocate income for things like day-to-day expenses and payroll. You can also use checking accounts to set up, separate and continually contribute to cash reserves for taxes, investments for growth and unexpected emergencies online or via our mobile banking app.

If you’re ready to open a business checking account, consider choosing Relay, as it will help you spend, save and plan more efficiently — with unparalleled clarity into operating expenses, cash flow and accounts payable. Head here to get started today!